The Denver residential market is slowing down, but still looking good for October! The 10-year average for new listings is 4,653 for the month of October, but we only saw 3,546 new listings this month. With low inventory and properties going under contract quickly, the months of inventory remained at 2 months. Mortgage interest rates with a 30-year term ended October at 7.76%. Let’s dive into the key market data for Denver residential real estate market to see what is happening with supply, demand, sales prices, and months of inventory for October 2023.

Supply

In October we had 6,996 new listings hit the market! This is down (16.1%) from September. Unfortunately, this is down (5.9%) compared to October 2022.

The total amount of active listings at the end of the month was 6,996. This is down (5.9%) from Oct 2022. The 10-year October average from 2013 to 2022 is 7,118 listings, so we are below our long-term average.

The most recent report for detached home construction starts is Sep 2023. The Denver Metropolitan Statistical Area (MSA) pulled permits on 723 homes. This is lower than the three year average of 2,279 for September. Year to date construction starts for 2023 compared to the same period in 2022 shows a (21.2%) decline.

All in all, the supply is in a better position compared to 2021 and 2022 but is still lower than 2019 and 2020.

Demand

Showings are a great leading indicator for demand in the residential real estate market. There were 41,401 showings booked through the largest showing service in the Denver metro area during October.

This is down (7.7%) when compared to Oct 2022 and down (8.3%) compared to Sep 2023. The average amount of showings for October, over the last four years, is 79,483.

Denver had 2,909 properties go under contract in October 2023. This is up 4.2% compared to September, but is down (0.6%) compared to Oct 2022.

There were 2,889 closings in Oct 2023 compared to 3,145 in Sep 2023. This is a (8.1%) decrease from last month. A year ago, we had 3,306 closings in Oct so the volume of closings is down (12.6%) YOY.

The median days on market for Oct 2023 increased to 31 days from 29 days in Sep. This means that the market is slowing down, houses are sitting on the market for about a month before they are sold.

The list price to close price ratio held steady at 100%, so sellers are generally getting what they are asking. With that said, I have seen homes that are over priced sit on the market for a long time.

All in all, demand for housing is soft when we look at showings but decent when we look at closings. Let’s look at the median sales price.

Sales Prices

The median sales price has slowly increased this year, but in the last month it has gone down. The median price in October was at $575,000, but compared to in September it was $580,000. This metric includes detached and attached properties. The median price has increased 0.9% over the last year.

The long-term average appreciation for residential real estate is 6%. Higher prices and higher interest rates will continue to temper appreciation in the short run. Tight inventory is helping to prop up the market.

This month, prices were up 0.9% from last year! Even though Oct 2023 is lower than Sep 2023, median sales prices are still rising above Oct 2022.

Let’s look at months of inventory now.

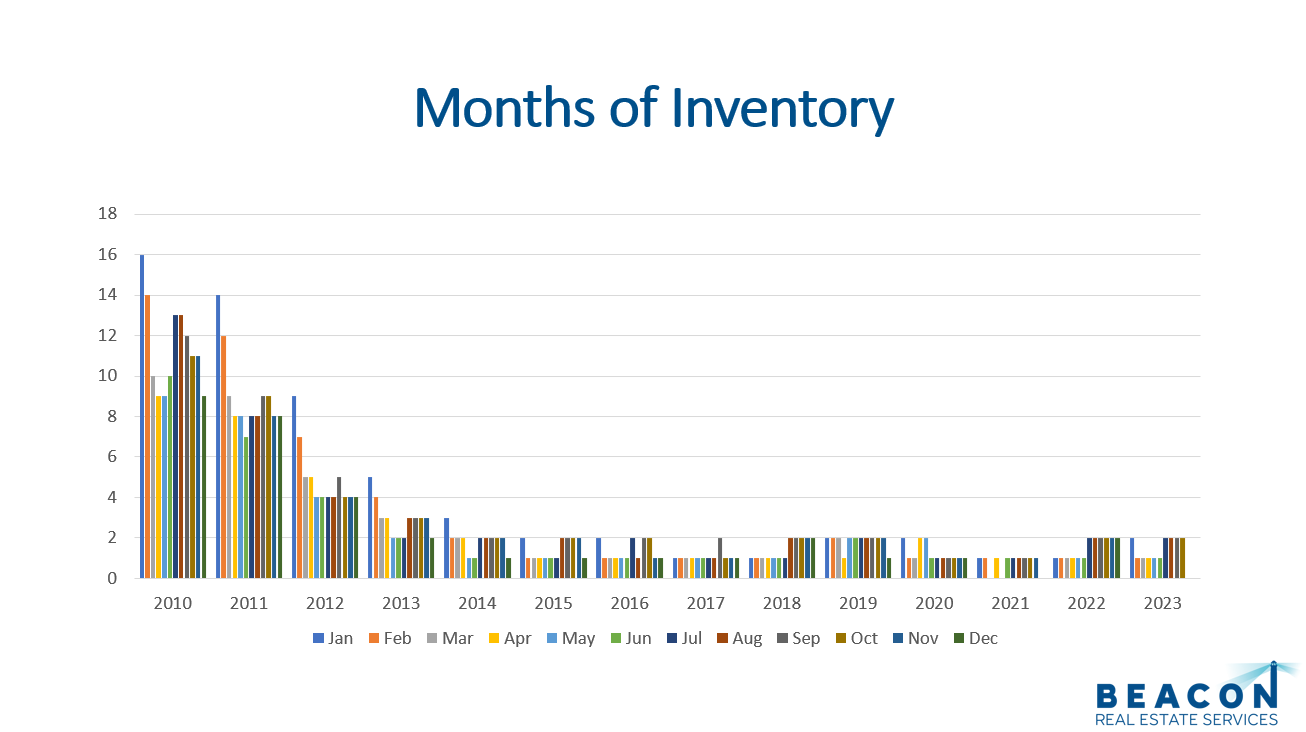

Months of Inventory

The months of inventory is a great indicator to watch for market trends. Typically, a seller’s market has 0-3 months of inventory. A balanced market has 4-6 months of inventory, and 7+ months of inventory is a buyer’s market. In a seller’s market prices go up. In a buyer’s market prices go down.

With 6,996 listings on the market and 2,889 closings in October, the months of inventory is at 2 months or 10.36 weeks of inventory. Therefore, the inventory is still low when compared to the demand. We expect the months of inventory to continue to be low this year.

All in all, months of inventory is a great metric to watch.

Final Thoughts

In conclusion, supply, demand, median sales price, and months of inventory are ideal key performance indicators to watch for market trends. Supply is higher than the record lows of 2021 and 2022 but is still lower than the long-term average. Overall demand is there, even with higher prices and higher interest rates. We believe there is a tremendous amount of pent up demand happening right now and as soon as rates come down, more buyers will enter the market. Lastly, 2 months of inventory still quite low.

Here is the link to the full presentation: Denver Metro Residential Market Update 2023.pdf